Welcome to the Chalten Investment Review for Q4 2025. Stock market performance during the quarter mirrored much of what we saw for 2025 as a whole. Canadian stocks performed strongest, followed by both developed and emerging International stocks followed by US stocks. Over the past few years we’ve grown used to US market leadership. Does the rotation away from US outperformance in 2025 signal a new trend? Does it signal a rotation away from the Magnificent 7 group of stocks? Time will tell!

To kick off 2026 we decided to look back at emails from clients at the beginning of 2025. There was a few common themes that emerged. First of all, there was a lot of concern about events south of the border and potential effects for Canada. This concern intensified as the US rolled out tariffs at the beginning of April and market volatility increased. And of course we just had two years of above average market performance so there was concern about markets coming down off “all time highs” and that “this time is different”. A regular topic of the Chalten Investment Review is the importance of staying the course and 2025 was a really important example of this. After a shaky start, market performance was very strong for the remainder of the year. We think it’s natural for investors to express their concerns and it’s our job to reinforce good behaviour! Professional market pundits and research analysts are paid to coerce investors into action. When the opportunity arises we aren’t averse to pointing out that they often get things very wrong. Welcome to our little “Shot and Chaser” segment of the Quarterly Review highlighting some of our favourite 2025 market predictions vs outcomes:

Shot: “The current polarized regional equity performance will likely persist going into 2025, with US equities preferred over eurozone and emerging markets”

Chaser: +15.2% Global ex-US markets outperformance vs US

Shot: “2025 will clearly be a case of strong economy, strong currency for the US dollar.”

Chaser: -5.97 % decline of US dollar vs other major developed market currencies on average

Shot: “China will be incapable of providing a sustainable economic recovery or a stock market breakout.”

Chaser: +8.8% China outperformance vs global markets

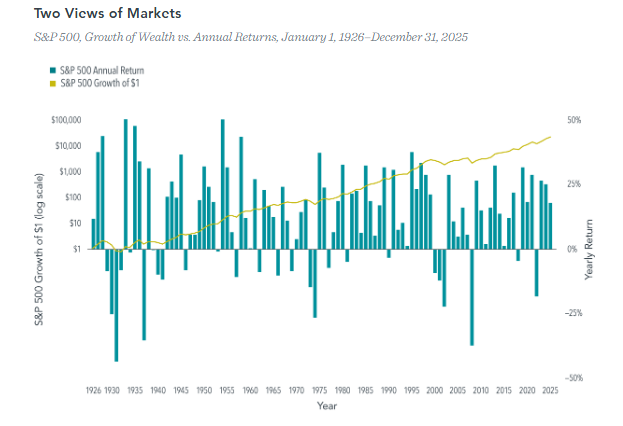

So what do we do now after a third year of strong market performance? Even fixed income returns have normalized – surely we’re due for a pull back? The answer, as usual, is to stay the course. That’s not to say that a good mental fire drill isn’t worthwhile to prepare us to behave properly when the eventual market downturn happens. Knowing the range of possible outcomes, and how to behave in those circumstances, is critical to success for the long-term investor. The odds are you’ll be tested with a downturn. We have US stock market data going back almost one hundred years and we observe the following:

- Stocks have experienced a >10% decline in more than half of all years (56 out of 98 years)

- Stocks have experienced a > 20% decline in almost a third of all years (29 out of 98 years)

- Stocks have experienced a > 30% decline in about 10% of all years (10 out of 98 years)

It’s important to keep in mind that a bad stretch doesn’t mean a bad year to come. While a 20% slide occurred in 29 years, only six times did the market end up below −20% for the full year. And the market actually posted positive full-year returns in 10 of those 29 years. This reinforces the lesson that the most reliable course of action following a market downturn is to remain invested.

We can’t control—or predict—market drops. What we can do is avoid compounding losses by reacting!

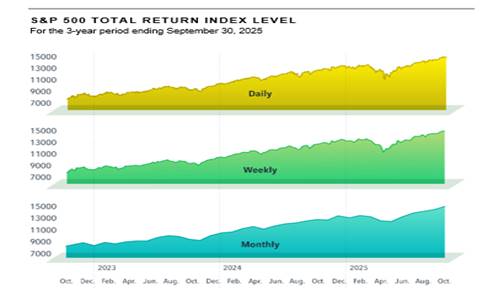

One thing that helps with staying the course (in addition to ignoring market pundits!) is looking through the inevitable day to day, month to month, and even year to year, volatility. As the following chart shows, the less often you look at the market, the smoother returns appear!

Even annual performance can be very volatile (see chart below from Dimensional Fund Advisors) and, as the above data shows, downturns happen. But if our allocation between safe and risky asset classes is appropriate for our risk tolerance and situation, staying the course gives us the best chance of achieving a good long-term investment experience!

Financial Planning topics of interest

As we begin the new year a few things to keep in mind:

- TFSA: The contribution limit for 2026 remains at $7,000 + any accumulated contribution room from prior years + amounts withdrawn in prior years. The total contribution limit if you’ve never had a TFSA is now $109,000. Beware of TFSA limits posted on your CRA account early in the year – these will not have been updated with the prior year’s activity yet!

- RRSP: Remember you can make contributions to deduct against your 2025 income up until March 2nd this year!

- Tax time: You will need to collect the relevant tax slips for investment accounts and dig up receipts for charitable contributions, eligible medical and educational expenses.

- Federal tax brackets: There are new federal tax brackets which are adjusted each year for inflation.

- For Q1 2026 the prescribed rate of interest for spousal loans remains at 3% which has been in place since the CRA dropped it from 4% in July of last year.

_______________________________________________________________________________

To conclude, we provide a summary of 2025 from Dimensional Fund Advisors: “A few big market swings, coupled with concern about how much additional volatility may be on the horizon, resulted in many occasions where investors may have considered making sudden changes to their investment portfolios in 2025.

Throughout the year’s ups and downs, Dimensional encouraged investors to stay in their seats, noting that history shows markets have overcome every previous challenge, eventually bouncing back from downturns. While an investor’s instinct may be to pull out money until things “calm down,” the impact of being out of the market for even a short period of time can be profound.The bottom line: Know the difference between thoughtful changes to portfolios based on your personal circumstances and hasty decisions driven by scary headlines. The first is smart financial planning; the second is more like gambling.”